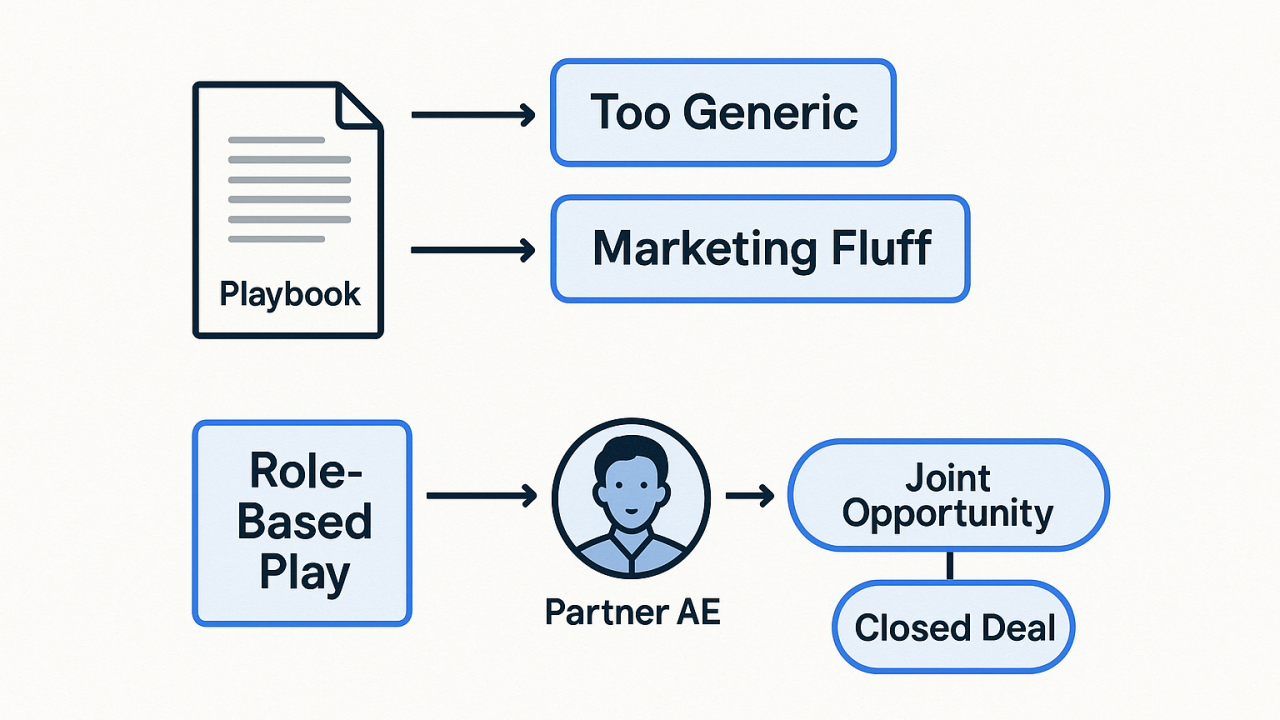

Stop “Teaching” Partners — Start Building Partner Muscles

For decades, partner enablement has rested on a simple assumption: if partners learn the technology, they’ll know how to sell and deliver it. That logic made sense when platforms were new and unproven. Partners needed education to understand whether the technology even worked.

That era is over.

In mature ecosystems like Salesforce, AWS, Microsoft, and Google Cloud, partners don’t join because the product might work. They join because it already does. The platform is validated. The value is clear. The risk is gone.

The power dynamic has flipped.

The ecosystem no longer needs partners to validate the platform.

Partners need to prove why they matter inside the ecosystem.

Most enablement models haven’t adjusted.

For decades, partner enablement has rested on a simple assumption.

If partners understand the technology, they will know how to sell and deliver it.

That logic made sense when enterprise platforms were new. Partners needed education to determine whether the product worked, how it fit into customer environments, and whether it was worth building a practice around.

That era is over.

In mature ecosystems such as Salesforce, AWS, Microsoft, and Google Cloud, partners do not join because the technology might work.

They join because it already does.

The platform is validated.

The value is proven.

The risk is gone.

The power dynamic has flipped.

The ecosystem no longer needs partners to validate the platform.

Partners need to demonstrate why they matter inside the ecosystem.

Most partner enablement models have not adjusted to this shift.

Traditional Partner Enablement Breaks at Ecosystem Scale

At small scale, traditional enablement works reasonably well.

With a few dozen partners:

Webinars are interactive

Partner managers provide hands-on guidance

Alignment happens inside real deals

But as ecosystems grow into the thousands of partners, the model begins to collapse.

Engagement drops—not because partners are uninterested, but because they are being taught things they already understand.

Most partners do not need to learn how the product works.

They need to learn how to win inside the vendor’s go-to-market system.

Those are fundamentally different problems.

Content Creates Familiarity. Repetition Creates Capability

When ecosystem leaders sense this gap, the default response is to produce more content.

More presentations.

More certifications.

More messaging sessions.

But content alone rarely creates partner readiness.

Content teaches partners what to say.

Repetition teaches partners what to do.

A webinar does not create co-sell competence

A certification does not build execution muscle

A slide deck does not produce repeatable sales motion

Capability is built through repetition, feedback, correction, and progression.

Partners do not need to hear the message again.

They need structured opportunities to apply the motion, encounter friction, and improve.

The Real Gap Is Sales Motion Clarity

Partnerships ultimately function as a form of sales collaboration.

Different audiences.

Different narratives.

The same fundamental requirement: a clear sales motion.

If a partnership does not sit inside a defined go-to-market motion, it cannot scale.

Most partners already understand how to deliver outcomes with the technology.

What they often lack is clarity around:

How to position their value in a way the vendor’s field sellers recognize

How to tell a customer story that aligns with the vendor’s deal cycle

Where their role begins and ends in the co-sell motion

How to move predictably through the partner-led sales process

Teaching words is not the same as teaching execution.

Scaling Ecosystems Requires Conditioning, Not Education

At ecosystem scale, the goal is not to enable every partner equally.

The goal is to build repeatable execution among partners capable of running the motion.

That requires systems rather than campaigns.

It requires:

Structured opportunities for partners to practice the motion

Feedback loops between partners and field sellers

Reinforcement of behaviors that produce successful deals

Signals that reveal which partners are progressing and which are not

Ecosystems rarely fail because partners lack information.

They fail because partners are not conditioned to execute consistently inside the vendor’s go-to-market model.

How PRTNRd Approaches Partner Enablement

At PRTNRd, we focus on helping enterprise SaaS companies move beyond content-driven enablement toward systems that build partner capability.

This includes designing partner activation programs that allow partners to run real co-sell motions, receive feedback, and refine their approach over time.

The goal is not simply to educate partners.

It is to help them develop the operational muscle required to execute inside complex partner ecosystems.

Final Thoughts

Partner ecosystems do not scale when partners are taught.

They scale when partners are built.

Ecosystem leaders who shift their focus from information coverage to execution capability will see stronger partner adoption, more consistent co-sell engagement, and more predictable partner-led revenue.

Stop optimizing for coverage.

Start optimizing for capability.

Pipeline Is a Lagging Indicator. Behavior Is the Leading One

Pipeline has long been treated as the ultimate source of truth in partner ecosystems. It’s measurable, reportable, familiar—and deeply misleading. Pipeline doesn’t tell you how partners perform. It tells you what happened after months of behavior already played out. In ecosystems with hundreds or thousands of partners, waiting for pipeline to reveal who’s worth investing in means you’re already late.

Pipeline has long been treated as the ultimate source of truth inside partner ecosystems.

It is measurable, reportable, familiar—and often deeply misleading.

Pipeline does not reveal how partners perform. It reveals what happened after months of behavior have already played out. By the time partner pipeline appears in dashboards or CRM systems, the underlying go-to-market motion has either succeeded or failed.

In ecosystems with hundreds or thousands of partners, waiting for pipeline to determine who deserves investment means you are already late.

The Real Problem Isn’t Partner Count — It’s Visibility

Many ecosystem leaders assume the solution is fewer partners and tighter focus.

The instinct is understandable, but the logic is backwards.

The problem is not partner quantity.

The problem is that pipeline-only visibility forces ecosystem teams to concentrate investment around the same top partners while overlooking others who could scale if the right signals were recognized early enough.

Pipeline shows outcomes.

Behavior shows trajectory.

Most ecosystems today have no reliable way to observe partner behavior at scale.

What Behavior-Led Ecosystem Scoring Measures

Behavior-led ecosystem management shifts focus away from outcomes and toward the motions that consistently precede them.

Instead of reacting to pipeline after deals emerge, behavior-led scoring identifies the early indicators that predict partner success.

Key behavioral signals include:

Clarity and repeatability of partner use cases

Specific definition of the ideal customer profile (ICP)

Maturity of the partner’s sales motion

Responsiveness during early interactions with account executives

Evidence of applied enablement rather than simple content consumption

Real specialization patterns across industries or technologies

Alignment between partner delivery teams and go-to-market positioning

Consistency of signals shared with the vendor’s field organization

These behaviors create the conditions that produce pipeline.

Pipeline itself is simply the downstream result.

Why Pipeline Breaks Down at Ecosystem Scale

As the primary metric for ecosystem health, pipeline begins to fail in predictable ways as ecosystems grow.

Pipeline appears slowly, often lagging by an entire fiscal cycle

It favors familiar partners repeatedly invited into deals by trusted sellers

Emerging partners doing everything right remain invisible until revenue appears

The bottom of the ecosystem becomes flattened, where zero pipeline looks identical for partners with potential and those without it

Behavioral insight helps distinguish “not yet” from “not ever.”

Without this distinction, ecosystem teams waste time evaluating the wrong partners and miss opportunities to incubate the right ones.

The Behavior → Pipeline Loop

Pipeline is not the starting point of partner success.

It is the final step in a longer chain of ecosystem behavior.

The pattern usually unfolds like this:

Strong go-to-market behavior builds trust with field sellers

Trust leads to early invitations into opportunities

Early invitations create visibility inside deals

Visibility produces partner pipeline

Pipeline converts into revenue

Pipeline is the output of a system.

It cannot be demanded.

It can only be engineered through the behaviors that precede it.

The Strategic Shift Ecosystem Leaders Are Making

Behavior-led ecosystem management enables partner teams to operate far more effectively at scale.

This approach makes it possible to:

Identify high-potential partners earlier in their lifecycle

Give partner managers objective guidance on where to focus

Operationalize readiness across all ecosystem tiers

Measure ecosystem health continuously rather than quarterly

These capabilities are becoming increasingly important as partner ecosystems expand and traditional relationship-based management models reach their limits.

How prtnrIQ Approaches Behavioral Ecosystem Intelligence

This shift toward behavioral ecosystem management is one of the principles behind prtnrIQ, the partner intelligence platform being developed by PRTNRd.

Instead of evaluating partners primarily through historical revenue performance, prtnrIQ focuses on signals of behavioral readiness and go-to-market maturity.

By identifying these signals earlier, ecosystem leaders can direct resources toward partners capable of scaling partner-led revenue before pipeline appears.

Final Takeaway

Pipeline still matters.

But it is a shadow, not the source.

Ecosystems that steer primarily by pipeline will remain reactive and concentrated around the same partners.

Ecosystems that manage by behavior will build predictable, scalable growth—by design rather than by accident.

From Enablement to Intelligence: The Evolution of Ecosystem Data

For two decades, partner enablement has been treated as a content problem: build it, upload it, and hope someone uses it. But ecosystems are now undergoing the same shift that transformed sales, marketing, and product—from knowledge, to behavior, to intelligence. Static libraries are giving way to adaptive systems that understand readiness, guide action, and surface signal long before revenue appears.

For more than two decades, partner enablement in SaaS ecosystems has been treated primarily as a content problem.

Create enablement materials. Upload them to a partner portal. Encourage partners to complete certifications. Host periodic webinars.

The assumption was simple: if partners had access to the right information, they would eventually use it.

But ecosystems are now undergoing the same transformation that reshaped sales, marketing, and product over the last decade—moving from knowledge systems to behavioral systems to intelligence systems.

Static enablement libraries are giving way to adaptive ecosystem intelligence platforms that can assess readiness, interpret behavior, and guide partner action long before revenue appears.

Why Traditional Partner Enablement Has Reached Its Limit

Most partner ecosystems still operate using a familiar enablement infrastructure:

Portals full of PDFs and documentation

Certification programs designed around product knowledge

Quarterly webinars and enablement campaigns

Internal notes scattered across Slack threads, spreadsheets, and email

The problem is not effort. Most ecosystem teams produce an enormous amount of content.

The problem is context.

Content distribution alone does not scale co-sell execution. It does not reveal which partners are ready for field engagement, which partners are stalled, or which partners require targeted intervention.

More importantly, content systems produce almost no usable ecosystem data.

By the time pipeline appears inside CRM systems, the underlying partner motion has already succeeded—or failed. Pipeline is an outcome metric, not a diagnostic one.

The Shift From Content Data to Behavioral Ecosystem Intelligence

Modern partner ecosystems require a deeper form of data: intelligence about how partners actually operate in the field.

This transition introduces three critical layers of ecosystem data.

1. Partner Readiness Scoring

The first layer evaluates whether a partner can realistically execute a go-to-market motion.

Partner readiness scoring typically analyzes structural signals such as:

Clarity of industry or use-case positioning

Definition of the ideal customer profile (ICP)

Maturity of the partner’s sales process

Quality of supporting GTM content and messaging

Evidence of specialization or domain expertise

Operational readiness within delivery teams

Readiness scoring replaces subjective partner evaluation with a measurable baseline. Instead of asking “Is this partner good?”, ecosystems begin asking “Is this partner structurally ready to execute?”

2. Behavioral Ecosystem Data

The second layer measures whether a partner is likely to execute in practice.

Behavioral ecosystem data tracks signals such as:

Engagement with AE-facing enablement materials

Responsiveness during early co-sell interactions

Adherence to recommended sales plays

Deal hygiene and opportunity discipline

Frequency and quality of partner-field interactions

These signals appear long before pipeline.

Behavioral insight allows ecosystem teams to identify emerging partners, detect friction in partner motions, and prioritize intervention where it will produce measurable lift.

3. AI-Driven Contextual Guidance

The third layer introduces adaptive intelligence.

Instead of waiting for partner managers to interpret signals manually, AI systems analyze behavioral and readiness data in real time and generate contextual guidance.

Examples include:

Flagging ICP mismatches in early-stage opportunities

Prompting partners to attach proof points before requesting introductions

Recommending co-sell plays based on similar partner wins

Highlighting readiness gaps that block partner engagement

Surfacing high-potential partners before pipeline appears

This turns partner enablement from a passive library into an active operating system for ecosystem collaboration.

Enablement no longer waits for partners to consume information. It interprets signals and guides action continuously.

How Ecosystem Intelligence Changes the Role of Partner Teams

Historically, partner managers acted as translators.

Partners would bring fragmented information about capabilities, deals, or positioning, and PAMs would manually convert that input into something the vendor’s sales team could use.

This work was valuable but inefficient.

In an intelligence-driven ecosystem model, much of that translation becomes automated.

AI evaluates readiness.

Behavioral data surfaces execution patterns.

Automated nudges guide partner actions in real time.

As a result, partner leaders can shift their focus toward higher-leverage activities:

Strategic ecosystem design

Prioritization of high-potential partners

Deep relationship development with anchor partners

Coordination with field sales leadership

The role becomes more strategic, not more administrative.

Why Ecosystems Cannot Ignore This Shift

The next generation of partner ecosystems will not be defined by partner counts or enablement volume.

It will be defined by intelligence.

Specifically:

Readiness intelligence that identifies which partners can execute

Behavioral intelligence that predicts which partners will execute

Adaptive enablement systems that guide execution continuously

Ecosystems that adopt intelligence-driven models will scale partner-led revenue predictably across hundreds or thousands of partners.

Ecosystems that remain dependent on static content libraries will continue to concentrate revenue among the same small group of visible partners.

Final Takeaway

Partner enablement is no longer about distributing information.

It is about interpreting behavior and guiding action at ecosystem scale.

The ecosystems that win will not necessarily have the largest partner networks or the most enablement content.

They will be the ecosystems that:

Understand partner readiness early

Detect behavioral signals quickly

Intervene intelligently

Turn ecosystem data into coordinated motion

Because in modern partner ecosystems, intelligence—not content—is what ultimately drives scalable partner-led growth.

The Death of Partner Portals: Why AI Agents Will Redefine Ecosystem Enablement

Partner portals have been the backbone of enterprise ecosystems for decades. They store content, certifications, deal registration, and program rules. They still matter. But they were never designed to enable partners—and at scale, that mismatch is breaking ecosystems.

Portals are backward-looking systems. They track what has already happened. Modern ecosystems, however, need guidance on what should happen next. That gap is where billions in partner-driven revenue quietly disappear.

Partner portals have been the backbone of enterprise partner ecosystems for decades.

They store enablement content, certifications, deal registration workflows, program requirements, and partner tiering rules. In most enterprise SaaS ecosystems, the portal functions as the operational center of the partner program.

Portals still matter.

But they were never designed to enable partners at scale.

They were designed to store information and manage program compliance. As partner ecosystems grow into the thousands or tens of thousands, that difference becomes increasingly visible. What ecosystems need today is not simply access to information. They need guidance, prioritization, and visibility into partner readiness.

This is where the traditional portal model begins to break.

Partner Portals Are Systems of Record, Not Systems of Guidance

Partner portals are inherently backward-looking systems.

They track what has already happened:

Certifications partners have completed

Deals partners have registered

Content partners have downloaded

Program tiers partners have achieved

These are useful operational signals.

But they are historical signals.

Modern partner ecosystems increasingly need something different: insight into what should happen next.

They need to know:

Which partners are ready to execute a co-sell motion

Which partners require targeted enablement to become viable

Which partners are likely to produce pipeline in the future

Where partner managers should focus limited attention

Traditional portals were never designed to answer these questions.

Why Partner Portals Work for Top Partners but Fail the Long Tail

The limitations of partner portals are most visible when ecosystems scale.

Top-tier partners tend to use portals effectively because they already understand how to operate inside the vendor’s ecosystem. They know which materials matter, how to position solutions, and how to navigate the co-sell process.

Long-tail partners experience something very different.

They log in once, encounter hundreds of documents, multiple certification paths, and complex program requirements, and quickly disengage.

Meanwhile, account executives rarely engage with partner portals at all. Their work happens inside the CRM. From their perspective, partners become relevant only when they demonstrate credibility and contribute to real opportunities.

This dynamic creates a structural gap:

Portals hold the information partners need

But they do not help partners translate that information into commercial action

The Hidden Opportunity Inside Large Partner Ecosystems

Every major SaaS ecosystem contains a long tail of partners generating modest annual contract value.

Many operate in the range of:

$1M in annual partner-sourced or influenced revenue

$5M in annual contributions

$10M in niche vertical opportunities

These partners rarely receive dedicated partner manager support. Yet many have the potential to scale significantly with the right guidance.

The problem is that portals do not surface this potential.

Portal metrics reveal activity, not readiness.

They show what partners studied or downloaded. They do not reveal whether a partner has:

A clear ideal customer profile (ICP)

A repeatable use case

A structured sales motion

The ability to position independently with field sellers

Without these signals, ecosystems struggle to distinguish between partners who could scale and partners who will remain peripheral.

Scaling Ecosystems Without Scaling Headcount

Partner managers should not attempt to support every partner equally.

High-touch orchestration is appropriate for strategic partners with large revenue impact. But large ecosystems also require a scalable way to guide the broader partner base.

What long-tail partners need is not constant human oversight.

They need structured progression.

This is where AI agents begin to reshape ecosystem enablement.

Rather than functioning as simple chatbots, ecosystem-trained AI agents can act as an intelligence layer across the partner base.

They can:

Help partners define and refine ideal customer profiles

Identify gaps in use cases or messaging

Recommend go-to-market motions aligned with vendor priorities

Surface readiness signals to ecosystem leaders

This approach allows ecosystems to guide thousands of partners without dramatically expanding partner manager headcount.

Why Account Executives Will Never Use Partner Portals

Another structural challenge with portal-led enablement is that the vendor’s sales organization rarely interacts with it.

Account executives do not build pipeline inside portals. They build pipeline inside CRM systems.

When evaluating partners, AEs rely on a small set of signals:

Credibility and expertise

Clarity of positioning

Evidence of past contribution

Alignment with customer needs

These signals rarely originate inside a portal.

AI-driven ecosystem intelligence can bridge this gap by translating partner readiness into signals visible within the sales workflow. By analyzing partner GTM materials, behavioral patterns, and ecosystem engagement, AI agents can surface which partners are truly ready for co-sell engagement.

From Static Portals to Adaptive Ecosystem Enablement

The next generation of ecosystem enablement will not eliminate portals.

Portals will continue to function as systems of record for compliance, certifications, deal registration, and program documentation.

But the operational center of enablement is shifting.

Instead of static content libraries, ecosystems are moving toward adaptive enablement systems that provide:

Partner readiness scoring

Behavioral insight across the partner base

Motion recommendations aligned with vendor priorities

Contextual guidance for partners during the co-sell process

In this model, the portal remains the repository of truth.

AI becomes the intelligence layer that turns that truth into actionable guidance.

Final Takeaway

Partner portals are not disappearing.

But portal-led enablement is.

As ecosystems grow larger and more complex, static content libraries cannot provide the guidance partners need to succeed. What ecosystems increasingly require is intelligence—systems that interpret readiness, detect behavioral signals, and guide partners toward effective go-to-market execution.

The ecosystems that adopt AI-driven enablement will be able to activate far more partners with far less manual effort.

Those that remain dependent on portal-based enablement will continue to concentrate revenue among a small group of established partners.

In modern ecosystems, information is no longer the bottleneck.

Guidance is.

And AI agents are quickly becoming the infrastructure that provides it at scale.

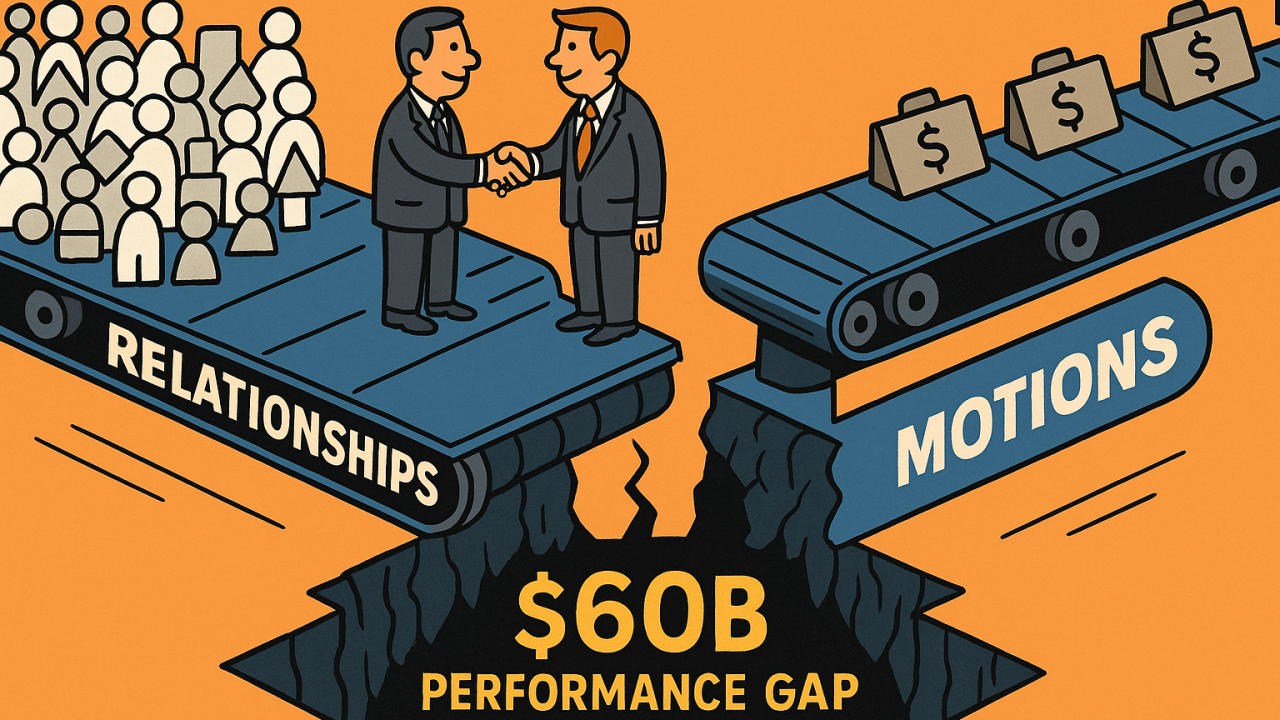

Why Your Partner Ecosystem Isn’t Performing: The $60B Problem

For years, vendors assumed their partner ecosystems were healthy because the same top partners kept delivering results. And if you only look at the top 50 or 100, that story still holds.

But widen the lens and a harder truth emerges: most partner ecosystems are underperforming—dramatically.

Across major platforms like Microsoft, Salesforce, AWS, Oracle, and Google Cloud, partner-driven economic activity exceeds $650B annually. Even a modest 5–10% performance gap caused by stalled motions, unclear positioning, and inconsistent activation translates into $30–60B in lost value every year. That gap shows up as slower ACV growth, weak attach rates, uneven co-sell performance, and thousands of partners who never reach their potential.

This isn’t a demand problem. It isn’t a technology problem. And it isn’t a partner supply problem. It’s an operating model problem.

For years, vendors assumed their partner ecosystems were healthy because the same top partners continued delivering results. If you only examine the top 50 or 100 partners in most enterprise SaaS ecosystems, that story still appears true.

But widen the lens and a more uncomfortable reality emerges: most partner ecosystems are underperforming—and by a large margin.

Across major platforms such as Microsoft, Salesforce, AWS, Oracle, and Google Cloud, partner-driven economic activity now exceeds $650B annually. Even a modest 5–10% performance gap caused by stalled commercial motions, unclear positioning, and inconsistent partner activation translates into roughly $30–60B in unrealized value each year.

That lost value appears in several places:

Slower annual contract value (ACV) growth

Weak solution attach rates

Inconsistent co-sell performance across regions

Thousands of capable partners who never reach commercial viability

This is not a demand problem.

It is not a technology problem.

And it is not a partner supply problem.

It is an operating model problem.

Ecosystems Outgrew Their Operating System

Enterprise SaaS ecosystems are still largely governed by a relationship-led model.

Success often depends on who you know inside the vendor organization, which account executives you can access, which executives sponsor you, and how frequently you appear at ecosystem events.

At small scale, this works.

But once ecosystems expand to 10,000, 20,000, or even 40,000 partners, the model collapses under its own weight.

As vendors reduced partner account manager (PAM) coverage without replacing the relationship layer with a structured motion layer, ecosystem performance began to fragment. The long tail of partners was pushed toward self-service portals. Mid-tier partners stalled. Field sellers defaulted to the few partners they already trusted.

Pipeline concentrated instead of expanding.

Relationships did not fail.

The operating model did.

The Real Gap Isn’t Knowledge, It’s Commercial Patterning

Most partners are not lacking technical enablement.

In fact, they are oversaturated with it.

Certification programs, technical bootcamps, architecture workshops, and solution documentation are abundant in nearly every enterprise ecosystem.

What partners often lack is commercial structure.

Partners may understand the technology extremely well, but they struggle to answer a more fundamental set of questions:

What specific customer problem do we solve repeatedly?

How should that solution be packaged commercially?

Where do we fit within the vendor’s co-sell motion?

Why should an account executive bring us into a deal?

What proof points support that positioning?

Technical enablement explains how a product works.

Commercial motions explain why customers buy.

Without a defined commercial motion, even technically capable partners struggle to generate consistent revenue.

Why Performance Collapses at Ecosystem Scale

When partners cannot clearly form or repeat commercial motions, ecosystems naturally drift toward survivorship bias.

The same small group of elite partners sources and closes the majority of deals. Mid-tier partners struggle to activate. Long-tail partners gradually disengage. Account executives default to familiarity instead of evaluating fit.

Over time, several patterns emerge:

Pipeline becomes concentrated among a small group of partners

Ecosystem diversity decreases despite large partner counts

Innovation slows because fewer partners participate in real deals

Revenue growth becomes dependent on a narrow set of relationships

What appears to be a thriving ecosystem from the outside is often far more fragile than it looks.

The Fix: Motion-Driven Ecosystems

Scalable partner ecosystems shift away from relationship-led coordination and toward motion-driven operating models.

Instead of relying on informal introductions and individual relationships, ecosystems begin to organize around structured commercial motions.

This includes:

Readiness scoring instead of static partner tiering

Motion assignment based on capability and specialization

Commercial enablement focused on repeatable use cases

Measurement tied to partner behavior rather than pipeline alone

Motions create clarity.

Clarity creates consistency.

Consistency creates performance.

And importantly, this model allows ecosystems to scale without dramatically increasing partner manager headcount.

Final Takeaway

The next generation of partner ecosystems will still rely on relationships—but relationships alone will no longer determine success.

As ecosystems grow larger and more complex, commercial motions become the true infrastructure of partner-led growth.

Relationships may open doors.

But only motions create revenue at scale.

Enablement Isn’t Education — It’s Behavior Change

For years, partner enablement has been treated as a knowledge problem. Vendors have invested heavily in training modules, certifications, and learning portals designed to make partners “know more.” Yet despite all that education, results remain uneven. Some partners accelerate quickly, while others stall—despite completing the same programs.

That’s because enablement isn’t about information. It’s about transformation.

Education changes what people know. Enablement changes what people do. In ecosystem sales, that difference determines whether partners generate pipeline or remain passive participants.

For years, partner enablement has been treated as a knowledge problem. Vendors invest heavily in training modules, certification tracks, and partner learning portals designed to help partners “know more.” The assumption is that once partners understand the technology, the ecosystem will naturally produce more pipeline.

But the outcomes rarely match the investment.

Some partners accelerate quickly. Others stall—even after completing the same training programs and certifications.

The difference isn’t knowledge.

It’s behavior.

Education changes what people know. Enablement changes what people do. In partner ecosystems, that distinction determines whether partners generate real pipeline or remain passive participants.

The Education Trap

Most partner programs stop at awareness.

Metrics such as attendance rates, certification completions, and course participation are easy to track, so they become proxies for enablement success. But those metrics only prove that information was delivered—not that it was applied.

Partners frequently leave enablement sessions with new presentations, new product knowledge, and new documentation. Yet their actual selling behavior remains unchanged.

They still qualify deals the same way.

They still pitch the same value.

They still hesitate to engage account executives differently.

This is the education trap: mistaking knowledge transfer for readiness.

True enablement only begins once partner behavior changes in the field.

From Learning Events to Behavioral Systems

Behavior change rarely happens through single learning events.

It requires a system designed around three conditions:

Repetition

Reinforcement

Relevance

Enablement cannot operate as a one-time training session or a linear certification path. It must function as an ongoing system that encourages application, feedback, and refinement over time.

Effective ecosystem enablement tends to follow a simple loop:

Introduce a specific sales behavior or commercial motion

Apply that motion in a real deal environment

Reinforce it through feedback, results, and field visibility

Scale the motion across similar partners or segments

Without reinforcement, education fades quickly.

With reinforcement, enablement becomes embedded in daily selling behavior.

Why Partner Enablement Is More Difficult

Behavioral enablement is especially challenging inside partner ecosystems.

Internal sales teams can be directed, measured, and managed through formal leadership structures. Partners operate differently. Each partner organization has its own incentives, priorities, and delivery models.

That means behavior cannot simply be mandated.

Partners adopt new motions only when they see a clear connection between new behaviors and meaningful outcomes.

Those outcomes usually include:

Faster deal cycles

Higher win rates

Stronger relationships with account executives

Greater visibility inside the ecosystem

Without a clear link between behavior and results, even high-quality enablement content goes unused.

The Shift in Measurement

Education measures participation.

Enablement measures adoption.

Forward-looking ecosystem leaders are beginning to evaluate enablement success through applied behavior rather than attendance metrics.

Examples of behavioral indicators include:

Co-sell motions executed after enablement sessions

Sales plays reused in live opportunities

Revenue velocity within partner cohorts that completed enablement

Frequency and depth of AE–partner collaboration

These signals reveal whether partners are changing how they operate—not simply what they know.

The New Imperative

The ecosystems that scale partner revenue most effectively treat enablement as behavior design.

They study what top-performing partners actually do in the field. They codify those actions into repeatable commercial motions. And they reinforce those motions until they become instinctive for other partners.

In this model, enablement is not about distributing knowledge.

It is about shaping behavior.

Because readiness is not a certificate.

It is a capability—and capabilities emerge from behaviors that repeat, refine, and scale across the ecosystem.

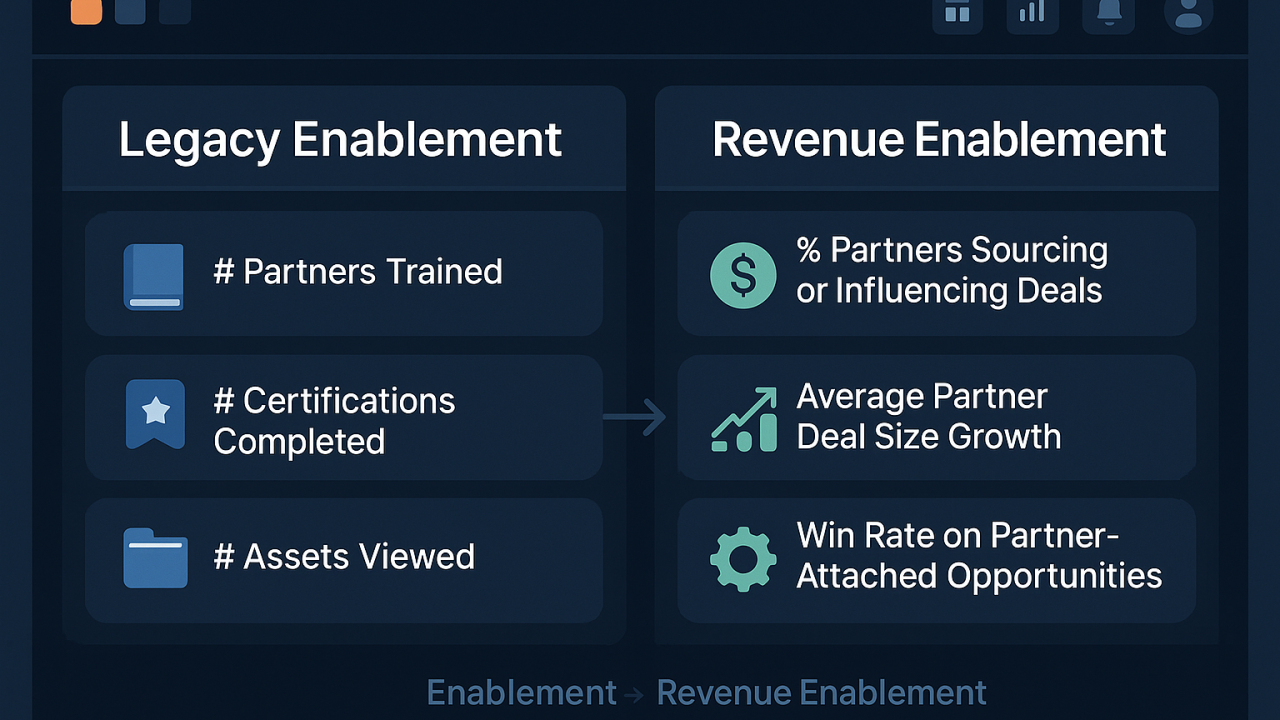

Stop Calling It Partner Enablement. Start Calling It Revenue Enablement.

If it doesn’t drive revenue, it’s not enablement. It’s education.

For years, partner enablement has been treated like a training function: content libraries, certifications, learning paths. Necessary? Yes. Sufficient? Not even close. In modern ecosystems, enablement that doesn’t translate into pipeline and closed deals is already obsolete.

If it doesn’t drive revenue, it isn’t enablement.

It’s education.

For years, partner enablement has been treated as a training function—focused on content libraries, certification tracks, and structured learning paths. These investments were meant to help partners understand the product and the ecosystem.

Necessary? Yes.

Sufficient? Not even close.

In modern SaaS ecosystems, enablement that does not translate into pipeline creation and closed deals is already obsolete.

Language Drives Funding—and Ownership

Words shape how organizations allocate resources.

“Enablement” often sounds like a support activity.

“Revenue enablement” signals growth responsibility.

That distinction matters because it determines both ownership and accountability.

Traditional partner enablement frequently sits under marketing or alliances teams. Its success is measured through activity metrics: how many partners completed training, how much content was consumed, and how many certifications were issued.

Revenue enablement shifts the center of gravity closer to sales and growth leadership.

Instead of asking how much information was delivered, organizations begin asking how much revenue partners helped create.

When the language changes, the mandate changes as well.

The KPI Shift: From Activity to Impact

Legacy partner enablement metrics focus on outputs:

Number of partners trained

Certifications completed

Assets viewed or downloaded

These indicators measure participation.

Revenue enablement focuses on outcomes:

Percentage of partners sourcing or influencing pipeline

Average deal size on partner-attached opportunities

Sales cycle reduction in co-sell deals

Win rates in opportunities where partners are actively involved

This represents a fundamental shift from awareness to activation.

The question is no longer what partners know.

The question is whether partners can sell with you.

Enablement as a Revenue Operations Discipline

When enablement is tied directly to revenue outcomes, it begins to resemble a revenue operations function rather than a training program.

At PRTNRd, enablement is approached through this lens.

Every enablement asset is designed to connect directly to execution in the field. Instead of distributing knowledge in isolation, enablement materials support specific commercial motions.

Examples include:

Use cases that define repeatable customer outcomes account executives can lead with

Accelerators that package services or solutions into offers capable of advancing deals

Sales plays that translate partner expertise into AE-ready motions inside real opportunities

When enablement is structured this way, partners stop operating as loosely connected specialists and begin functioning as extensions of the sales force.

Unlocking Real Investment

Linking enablement to measurable revenue outcomes also changes how organizations fund ecosystem programs.

When enablement is measured through participation metrics, it is often treated as a support cost.

When enablement demonstrates clear revenue contribution, it begins to attract real investment—additional headcount, better tooling, and increased automation.

This is why leading ecosystem platforms increasingly track indicators such as:

Partner-sourced pipeline

Partner-influenced annual recurring revenue (ARR)

Expansion revenue within accounts involving partners

These metrics reveal which partners are driving measurable commercial impact.

Partners who contribute consistently receive more investment. Those who do not gradually fall out of focus.

The Bottom Line

The next generation of partner programs will not celebrate certification counts.

They will reward contribution.

In an ecosystem shaped by AI-assisted insights and increasingly rich partner data, enablement can no longer function as a support layer. It must operate as a revenue function—connected directly to pipeline creation, deal acceleration, and customer expansion.

Organizations that recognize this shift will treat enablement as part of their growth infrastructure.

Those that do not will continue funding education programs that never translate into revenue.

Ecosystem Strategy Is Now a CEO Problem

For years, partnerships lived on the margins—adjacent to sales, loosely tied to marketing, and measured more by relationships than revenue. That era is over.

Ecosystem strategy has moved from a support function to a leadership mandate. Today, it’s a primary determinant of whether a SaaS company scales—or stalls.

For years, partnerships lived on the margins of enterprise software organizations. They sat adjacent to sales, loosely connected to marketing, and were often evaluated through the strength of relationships rather than the strength of revenue contribution.

That era is ending.

Ecosystem strategy has moved from a supporting role to a leadership mandate. In modern SaaS companies, the structure and maturity of the ecosystem increasingly determine whether the business scales efficiently—or stalls under the weight of customer acquisition costs and limited reach.

For many organizations, this shift is only now becoming visible.

But the companies that recognize it early are already reorganizing around it.

The New GTM Hierarchy

In enterprise SaaS, ecosystems are no longer optional distribution channels.

They have become the operating system for growth.

Modern go-to-market motions increasingly depend on partner coordination, including:

Co-sell programs with hyperscalers

Marketplace discovery and procurement

Joint industry solutions built with system integrators

Embedded integrations across platforms

Multi-partner solution architectures for complex customers

These motions are no longer experimental initiatives. They are how companies reach customers, win deals, and expand accounts.

Put plainly, ecosystem strategy is no longer a subset of GTM strategy.

It is GTM strategy.

The CEOs who recognize this shift are already adjusting their operating models by:

Elevating ecosystem leadership to executive-level ownership

Embedding partner-influenced revenue metrics into board reporting

Aligning ecosystem investment directly to growth outcomes rather than partner goodwill

When ecosystem performance becomes visible at the executive level, it begins shaping company strategy.

Why CEOs Can’t Delegate Ecosystem Strategy Anymore

Ecosystems now intersect with nearly every major strategic decision inside a SaaS company.

Consider how deeply partnerships influence core business functions:

Pricing: Marketplace economics and co-sell incentives influence competitive positioning

Product: Integration depth often determines customer stickiness and expansion potential

Marketing: Partner narratives extend credibility and distribution reach

Sales: Ecosystem readiness directly affects pipeline velocity and deal execution

AI strategy: Shared data and model collaboration increasingly shape competitive advantage

These dynamics cannot be optimized within isolated departments.

And they cannot be fully delegated.

When ecosystem leadership sits solely within sales or marketing organizations, investment often becomes fragmented. Product decisions move in one direction, sales incentives move in another, and partner strategy struggles to stay aligned.

Executive ownership ensures that ecosystem strategy remains integrated across the company.

Investor Expectations Are Changing

Investors and analysts are also beginning to view ecosystem maturity as a signal of scalability and long-term defensibility.

Growth-stage SaaS companies are increasingly evaluated on how effectively they leverage partners to extend their reach and reduce customer acquisition costs.

Firms such as IDC and ICONIQ Capital have highlighted partner leverage as an indicator of growth efficiency—not simply revenue volume.

As a result, the questions investors ask are evolving:

What percentage of revenue is partner-influenced or partner-sourced?

How differentiated is the company’s ecosystem compared with competitors?

How effectively does the ecosystem accelerate expansion within existing accounts?

Ecosystems are no longer viewed as optional channel programs.

They are becoming a valuation lever.

Partnerships as Infrastructure

In mature SaaS companies, ecosystems increasingly function as foundational infrastructure.

Much like CRM systems unified customer information and cloud platforms unified computing resources, partner ecosystems unify the broader market around a platform.

The competitive moat is no longer defined solely by product capability.

It is increasingly defined by the network surrounding the product:

Partners delivering services and implementation

Integrations extending functionality

Joint solutions addressing industry-specific problems

Shared data flows that increase switching costs

In this environment, the ecosystem itself becomes part of the company’s core architecture.

The Bottom Line

The next generation of SaaS leaders will not scale alone.

They will scale through ecosystems that are deliberately designed, actively governed, and owned at the highest level of the organization.

In a platform-driven economy—accelerated by AI, marketplaces, and integrated solution stacks—ecosystem strategy has become too important to remain a departmental responsibility.

It now sits squarely at the center of company leadership.

Ecosystem strategy is no longer just a partnerships problem.

It is a CEO problem.

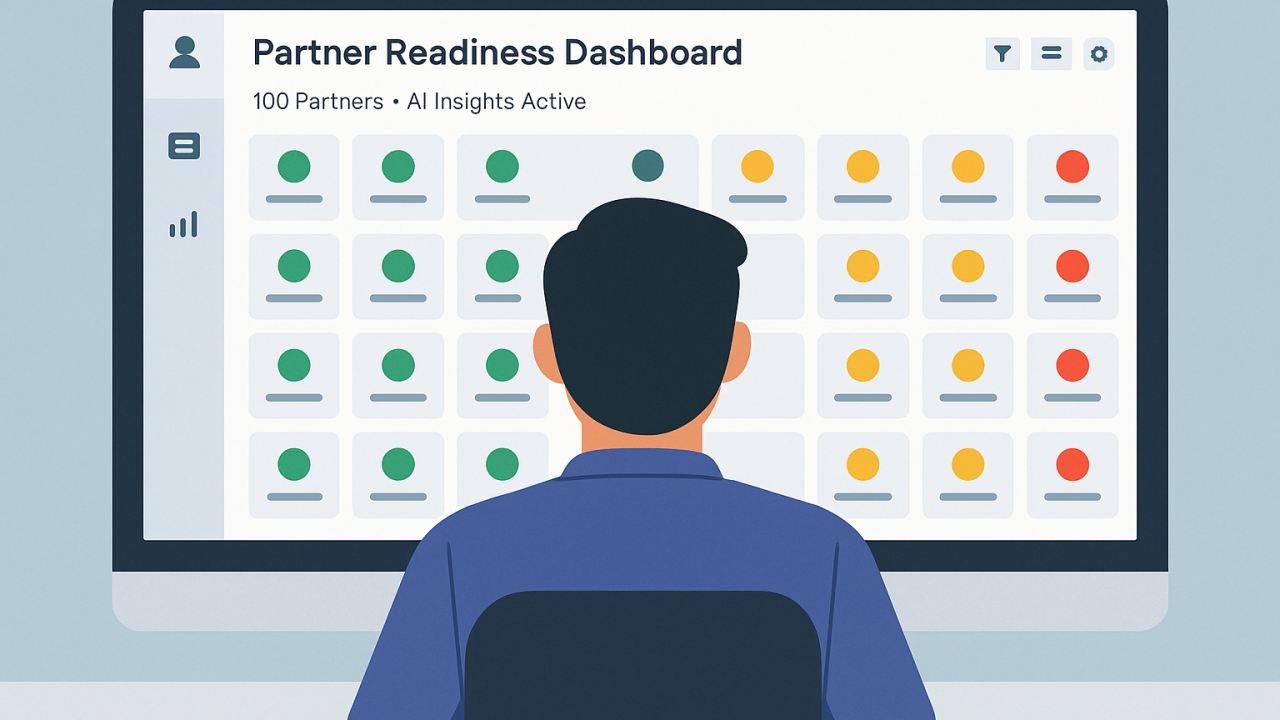

The Future of PAM Productivity: One Manager, One Hundred Partners—Without Chaos

For years, partner account management has been a math problem that never worked. A strong PAM can meaningfully support maybe 10 to 15 active partners—if the scope is clear and the system cooperates. Yet most ecosystems contain hundreds or thousands of partners. The result is familiar: reactive management, neglected mid-tier partners, and spreadsheets standing in for strategy.

The issue was never effort. It was tooling.

That equation is now changing.

For years, partner account management has been a math problem that never quite worked.

A strong Partner Account Manager (PAM) can meaningfully support roughly 10 to 15 active partners—assuming the scope is clear and the ecosystem itself is functioning well. Yet most enterprise ecosystems contain hundreds or thousands of partners.

The result is predictable:

Reactive partner management

Neglected mid-tier partners

Heavy reliance on spreadsheets and manual tracking

The issue was never effort.

Partner managers are often highly capable operators. The real limitation has been tooling and visibility. Without systems capable of surfacing readiness, engagement, and motion signals at scale, the only workable model was intensive focus on a small subset of partners.

That equation is now beginning to change.

Why the Model Finally Scales

AI-assisted partner management does not simply make the role easier. It makes it operationally possible at ecosystem scale.

When readiness signals, engagement patterns, and enablement pathways are surfaced automatically, the workload shifts from manual monitoring to intentional orchestration.

Instead of constantly asking, “What are my partners doing?” PAMs can begin asking a more strategic question:

Who is ready for what?

Modern ecosystem intelligence systems can now help identify:

Which partners are actually ready to engage in co-sell motions

What type of enablement each partner needs next

Where alignment with account executives will generate the highest return

When partner momentum is building—or quietly stalling

When machines handle pattern recognition, partner managers can focus on the areas where human judgment matters most: prioritization, strategic direction, and relationship leverage.

From Reactive Oversight to Predictive Management

The most significant shift is not simply scale—it is posture.

Traditional partner management is largely reactive. PAMs rely on status updates, reports, and pipeline signals that arrive long after underlying behaviors have already played out.

Predictive ecosystem signals allow managers to intervene earlier.

This enables partner leaders to:

Identify rising partners before their breakout moments

Step in when engagement or momentum begins to drift

Match partners to opportunities based on capability and fit

Trigger targeted enablement before deals are lost

In this model, AI does not replace the human layer of partnerships.

It sharpens it.

Instead of replacing relationships, AI helps identify where those relationships will create the greatest leverage.

What the PAM Role Becomes

As ecosystems become more data-informed, the role of the partner manager evolves as well.

The future PAM is not primarily an administrator managing partner accounts.

They are a growth operator managing commercial motion.

Their value is no longer defined by how many partners they check in with each quarter. It is defined by how effectively they convert partner readiness into real pipeline and revenue.

The job shifts from coordination to orchestration.

Less time spent gathering updates.

More time spent making signal-based decisions.

The Metrics That Replace Busywork

As the role changes, the metrics used to evaluate partner managers will change as well.

Instead of measuring activity, ecosystems will begin focusing on indicators tied to acceleration and impact.

Examples include:

Partner activation velocity

Time required to reach co-sell readiness

Revenue generated per partner manager

Pipeline generated within managed partner cohorts

Metrics such as partner counts, tier assignments, and manual reporting will gradually fade into the background.

Acceleration—not activity—becomes the measure of effectiveness.

The Bottom Line

AI will not replace partner managers.

But it will replace manual partner management.

The future of PAM productivity is not about increasing workload. It is about applying human judgment exactly where it creates the most value.

One manager supporting one hundred partners without chaos becomes possible—not because ecosystems shrink, but because the systems guiding them finally become intelligent enough to scale.

The Future of Partner Ecosystems Is AI-Led—But Only If Partners Are Ready

When enterprise SaaS leaders talk about AI-led ecosystems, they’re pointing to a real shift. The next competitive frontier isn’t just product adoption or industry specialization—it’s how effectively ecosystems can use AI to match partners to opportunities, surface insight, and scale execution.

But there’s a problem most teams underestimate: AI doesn’t fix weak systems. It accelerates whatever already exists.

If an ecosystem is fragmented, inconsistent, or unstructured, introducing AI won’t create clarity. It will amplify noise.

When enterprise SaaS leaders talk about AI-led ecosystems, they are pointing to a real shift. The next competitive frontier is no longer defined solely by product adoption or industry specialization. It is increasingly defined by how effectively ecosystems use AI to match partners to opportunities, surface insight, and scale execution across large partner networks.

But there is a constraint many organizations underestimate.

AI does not fix weak systems. It accelerates whatever already exists.

If an ecosystem is fragmented, inconsistent, or structurally unclear, introducing AI will not create clarity. It will amplify the existing noise.

Why AI Exposes—Not Solves—Ecosystem Gaps

Artificial intelligence performs best when patterns exist.

It depends on structured inputs, repeatable motions, and measurable outcomes. These elements allow algorithms to detect signals, identify correlations, and generate useful recommendations.

Many partner ecosystems lack those fundamentals—especially across mid-tier and long-tail partners.

As a result, AI initiatives inside ecosystems often stall or underperform. The technology itself is rarely the issue. The underlying readiness of the ecosystem is.

Several gaps appear repeatedly across large SaaS partner networks.

1. Undefined Go-to-Market Motions

Many partners possess strong technical delivery capabilities but struggle to articulate their commercial motion.

Questions that should be clear often remain vague:

Who is the ideal customer profile (ICP)?

What specific problem does the partner solve repeatedly?

Why is the partner differentiated from others in the ecosystem?

Without a clearly defined use case and market context, AI systems have nothing meaningful to surface or recommend.

Signal requires structure.

2. Lack of Packaged Offers

AI-driven ecosystems work best when partner offerings are structured.

Many services firms still sell “time and talent” rather than defined entry points. When services are not packaged into accelerators, solution bundles, or repeatable plays, they become difficult to categorize, recommend, or match with opportunities.

Unpackaged services tend to disappear inside AI-driven discovery environments.

Structure makes partners visible.

3. Inconsistent Sales Execution

Co-sell only scales when commercial motions are repeatable.

If every deal follows a completely different path—different positioning, different entry points, different delivery models—AI cannot identify patterns or optimize engagement.

Without consistency in execution, automation simply scales the chaos.

Predictability is what makes AI useful.

4. Weak Outcome Measurement

AI systems improve through feedback loops.

They learn from outcomes such as:

Reduced deal cycle times

Increased revenue within accounts

Cost savings delivered to customers

Expansion opportunities created after initial engagements

When these outcomes are not captured consistently, there is no reliable data to train models on and no signal strong enough to guide recommendations.

Measurement creates learning.

What Ecosystem Readiness Actually Requires

Closing these gaps requires a shift in how many partners—especially services firms—operate inside modern ecosystems.

Increasingly, successful partners behave less like traditional service providers and more like product organizations.

Key readiness capabilities include:

Define the market clearly: Identify the ideal customer profile, the core problem being solved, and the buyer context.

Codify the offer: Create a packaged entry point that can be reused across multiple deals.

Separate entry from expansion: Standardize how engagements begin, even if they evolve into customized solutions later.

Measure outcomes consistently: Capture results in ways that both sellers and customers recognize as credible.

These practices create the structured signals that AI systems can interpret and amplify.

Why This Matters Now

Ecosystem-led growth is already outpacing direct sales in many technology markets.

Customers increasingly buy solutions assembled from multiple partners rather than standalone products. Vendors rely on ecosystems to extend reach, deliver specialized services, and accelerate adoption across industries.

AI will only intensify this shift.

But ecosystems that attempt to layer AI on top of unstructured partner networks will train those systems on inconsistency—and receive inconsistent results in return.

The Bottom Line

The future of partner ecosystems will almost certainly be AI-assisted.

AI will help match partners to opportunities, guide enablement, surface insight, and orchestrate co-sell motions across thousands of partners.

But AI can only scale what is already disciplined.

If partner readiness, commercial structure, and measurable outcomes are not in place, AI will simply magnify the gaps.

Readiness is not optional.

It is the prerequisite for AI-led ecosystems.

Ecosystem ROI: Measuring the Impact of the Long Tail

In most ecosystems, the math is familiar: a small percentage of partners generate the majority of revenue. That reality often leads leadership to concentrate investment at the top and quietly deprioritize the rest. But the real question isn’t whether the long tail is smaller—it’s whether it’s measurable.

When long-tail impact isn’t visible, it’s treated as optional. When it is visible, it becomes defensible.

The problem isn’t a lack of value. It’s a lack of signal.

In most ecosystems, the math is familiar: a small percentage of partners generate the majority of revenue. That reality often leads leadership to concentrate investment at the top and quietly deprioritize the rest. But the real question isn’t whether the long tail is smaller—it’s whether it’s measurable.

When long-tail impact isn’t visible, it’s treated as optional. When it is visible, it becomes defensible.

The problem isn’t a lack of value. It’s a lack of signal.

What ROI actually looks like in the long tail

Measuring long-tail performance doesn’t require complex attribution models. It requires consistency and a focus on indicators that show momentum before revenue fully materializes.

1. Cost-to-serve versus pipeline lift

Start with basic economics. Track how much is being spent on a partner—enablement hours, MDF, programs—against the pipeline they influence or create. A partner driving meaningful pipeline with modest support is high ROI, even if they aren’t a top-tier producer yet. This metric surfaces efficiency, not just volume.

2. Marketplace velocity as a leading indicator

Marketplace activity often shows traction before pipeline does. Transactions, repeat usage, and solution adoption signal that a partner’s offering resonates and can scale. For long-tail partners, this is often the earliest proof that activation efforts are working.

3. AE adoption and pull-through

Revenue follows behavior. Which partners are AEs actually inviting into deals? Referral frequency, deal participation, and repeat engagement reveal far more than certifications or portal activity. If sellers are pulling a partner into accounts, trust—and ROI—are forming.

Why these measures matter

Research consistently shows that ecosystems activating mid-tier and long-tail partners outperform those focused exclusively on the top tier. Broader partner alignment correlates with higher pipeline growth and stronger customer retention, linking long-tail contribution to durable revenue rather than one-off wins.

What SaaS companies should do next

1. Make cost-to-serve visible

Create transparency around enablement spend and program investment, then map it directly to pipeline influence.

2. Build simple, repeatable dashboards

Track a small set of metrics—partner readiness progression, Marketplace activity, and AE involvement—across the long tail. Consistency matters more than precision.

3. Reinvest based on velocity, not labels

When long-tail partners show momentum, double down. Shift incremental investment toward those converting support into signal.

The takeaway

Ecosystem ROI isn’t proven by celebrating the top 10%. It’s proven by showing that the rest can move the needle when activated intelligently. When vendors measure cost-to-serve, Marketplace velocity, and AE adoption, the long tail stops being an expense line—and starts becoming a growth lever worth fund

The AE Trust Gap: Why Co-Sell Readiness Isn’t Enough

Every ecosystem leader has seen this play out. A partner checks all the boxes: packaged use cases, defined ICPs, certifications, even a few early co-sell motions. On paper, they’re ready. But in the field, nothing happens. AEs hesitate. Pipeline doesn’t move. The partner wonders why all that enablement never turned into deals.

The issue isn’t readiness. It’s trust.

Co-sell readiness gets a partner eligible. Trust gets them invited.

Every ecosystem leader has seen this play out. A partner checks all the boxes: packaged use cases, defined ICPs, certifications, even a few early co-sell motions. On paper, they’re ready. But in the field, nothing happens. AEs hesitate. Pipeline doesn’t move. The partner wonders why all that enablement never turned into deals.

The issue isn’t readiness. It’s trust.

Co-sell readiness gets a partner eligible. Trust gets them invited.

What actually builds AE trust

Across SaaS ecosystems, four factors consistently determine whether AEs engage a partner in real deals:

1. Proof of execution

Certifications signal capability, but execution creates belief. Five to ten visible joint wins matter far more than a long list of badges. Once AEs see a partner succeed in real accounts, momentum builds quickly.

2. Clear, deal-level outcomes

AEs don’t sell frameworks or features. They sell outcomes: reduced risk, faster cycles, revenue expansion. Partners that can explain their impact in one breath—what changed, by how much, and why it mattered—earn credibility faster than those relying on generic positioning.

3. Executive sponsorship

Partners backed by regional or segment leadership don’t wait to be discovered. When VPs or RVPs advocate for a partner, AEs interpret that as a signal that engagement is safe, supported, and worthwhile.

4. Field visibility

Trust spreads socially. Internal referrals, win wires, and shared calls make partners visible beyond a single deal team. When AEs hear about a partner from peers—not just partner managers—adoption accelerates.

Why the data supports this

Sales teams consistently report hesitancy engaging unfamiliar partners without a clear path to a win. Partners with active AE advocacy close materially more joint deals than those without. In practice, even a small number of referenceable wins can shift a partner from ignored to indispensable, unlocking outsized increases in field referrals.

What vendors should do differently

1. Measure trust, not just readiness

Readiness scores show preparation. Trust signals show adoption. Track AE referrals, repeat invitations, and leadership sponsorship alongside certifications and enablement completion.

2. Equip AEs with usable proof points

Replace abstract messaging with outcome-driven language AEs can use immediately in customer conversations.

3. Amplify trusted partners visibly

Highlight partners with real field traction. When trust is made visible, it compounds.

The takeaway

Readiness opens the door. Trust gets partners into the room. Ecosystems that stop at readiness leave value stranded. Those that intentionally build and measure trust turn prepared partners into consistent pipeline contributors. At scale, ecosystems don’t grow on enablement alone—they grow on belief.

From Chaos to Cohorts: Structuring Partner Growth at Scale

As SaaS ecosystems grow into the thousands—or tens of thousands—of partners, the challenge stops being growth and starts being focus. Most vendors know their top 10% well. Beyond that, the middle blurs together. Enablement becomes generic. AEs lose confidence in who to trust. Capable partners stall without clear direction.

The issue isn’t underinvestment. It’s lack of structure.

Managing partners one by one doesn’t scale. But treating everyone the same doesn’t work either. Cohorts solve this by turning an unmanageable long tail into an organized system for activation.

As SaaS ecosystems grow into the thousands—or tens of thousands—of partners, the challenge stops being growth and starts being focus. Most vendors know their top 10% well. Beyond that, the middle blurs together. Enablement becomes generic. AEs lose confidence in who to trust. Capable partners stall without clear direction.

The issue isn’t underinvestment. It’s lack of structure.

Managing partners one by one doesn’t scale. But treating everyone the same doesn’t work either. Cohorts solve this by turning an unmanageable long tail into an organized system for activation.

Why cohorts outperform one-to-one management

Cohorts group partners by what actually matters to execution, not just tier labels. Done well, they create leverage.

1. Maturity-based cohorts

Early-stage partners need positioning and packaging. Mid-stage partners need demand and co-sell motion. Advanced partners need pipeline alignment and sponsorship. Grouping by maturity ensures partners get what they need now, not what worked six months ago.

2. Vertical-based cohorts

Healthcare, financial services, energy, and public sector all sell differently. Vertical cohorts allow plays, messaging, and objections to be addressed once—then reused across dozens of partners. This gives AEs clarity and reduces friction in live deals.

3. Capability-based cohorts

Staffing firms, solution builders, and advisory-led partners shouldn’t be enabled the same way. Cohorting by delivery model aligns investment with how revenue is actually created.

Instead of spreading resources thin across hundreds of partners, cohorts let vendors drive repeatable outcomes across groups of 10–25 at a time.

What the data shows

Research consistently supports this approach. Vendors that structure enablement by vertical see significantly faster pipeline conversion than those relying on generic plays. Ecosystems that cohort mid-tier partners into structured programs show materially higher engagement than those using ad hoc outreach. In practice, grouping partners around a shared motion often produces more AE adoption than managing those firms individually.

How to implement cohorts without overengineering

Segment beyond tiers

Move past bronze/silver/gold labels. Use behavioral signals—GTM clarity, repeatable use cases, AE advocacy—to form cohorts that can act.Design cohort journeys

Map enablement to stages: awareness → activation → acceleration. Not every cohort needs the same depth or cadence.Measure at the cohort level

Track pipeline created, AE referrals, and win velocity across the group. Cohort metrics surface what’s working faster than partner-by-partner reporting.

The takeaway

Scale without structure creates chaos. Cohorts bring order. They allow ecosystems to focus effort, compress time to impact, and create visible momentum for both partners and the field. The vendors that win won’t be those with the most partners—but those that turn partner sprawl into coordinated growth.

Managing the “Unmanaged”: Turning Partner Shadows into Pipeline

At scale, partner ecosystems become a paradox. Platforms like Databricks and Snowflake support thousands of SIs, ISVs, and boutique firms building solutions, serving regional markets, and driving adoption. The reach is enormous. The coverage isn’t.

Once ecosystems mature, revenue concentrates quickly. A small percentage of partners receive direct attention, while the majority fall into an “unmanaged” category. In practice, that label doesn’t mean unqualified. It usually means under-scored, under-activated, and operating without a clear path to impact.

The problem isn’t partner quality. It’s calibration.

At scale, partner ecosystems become a paradox. Platforms like Databricks and Snowflake support thousands of SIs, ISVs, and boutique firms building solutions, serving regional markets, and driving adoption. The reach is enormous. The coverage isn’t.

Once ecosystems mature, revenue concentrates quickly. A small percentage of partners receive direct attention, while the majority fall into an “unmanaged” category. In practice, that label doesn’t mean unqualified. It usually means under-scored, under-activated, and operating without a clear path to impact.

The problem isn’t partner quality. It’s calibration.

Why “unmanaged” is the wrong frame

Long-tail partners often include:

ISVs building niche solutions in regulated or verticalized markets

Regional SIs trusted by customers early in the buying cycle

Boutiques that innovate quickly but lack co-sell context

These partners don’t need white-glove management. They need structure that matches their maturity. Without it, capable partners remain invisible—not because they can’t contribute, but because no one has translated where and how they fit.

What signals matter in the long tail

High-potential partners at the top of the ecosystem show clear GTM alignment, use cases, and early pipeline. Long-tail partners require a different lens. Useful signals include:

Clarity of focus: Do they know who they sell to and why?

Realistic ambition: Are goals achievable given their size and motion?

Honest capability definition: Do they understand where they add value—and where they don’t?

Outcome awareness: Are they tracking pipeline, marketplace activity, or repeatable wins?

These behaviors indicate whether a partner can be incubated into co-sell readiness.

The coverage math doesn’t work—and never will

Most partner managers support far more accounts than effective engagement allows. Headcount alone cannot scale to thousands of partners, even in well-funded ecosystems. As a result, the top tier gets deeper investment, while everyone else relies on portals, training libraries, and broad campaigns. It’s efficient—but it leaves meaningful pipeline untouched.

A more scalable operating model

Activating the long tail requires a different approach:

Stage-based enablement that adapts to partner maturity

Pre-packaged plays tied to real use cases and verticals

Partner scoring that routes attention based on behavior, not tier

The goal isn’t to manage more partners. It’s to graduate the right ones.

The takeaway

Unmanaged partners aren’t unmanageable. With the right signals, structure, and sequencing, they become the feeder system for marketplaces, field engagement, and future top-tier contributors. Ecosystems scale not by adding logos—but by activating intelligence where potential already exists.

How to Identify and Elevate High-Potential Partners

Not every partner deserves the same level of investment. In large SaaS ecosystems, trying to fast-track everyone spreads resources thin and rarely produces results. The vendors that scale partner-led revenue most effectively are selective. They focus on partners that show clear signals of readiness, momentum, and field trust.

High-potential partners don’t announce themselves through tier status alone. They reveal themselves through behavior.

Not every partner deserves the same level of investment. In large SaaS ecosystems, trying to fast-track everyone spreads resources thin and rarely produces results. The vendors that scale partner-led revenue most effectively are selective. They focus on partners that show clear signals of readiness, momentum, and field trust.

High-potential partners don’t announce themselves through tier status alone. They reveal themselves through behavior.

Four signals that predict partner success

1. GTM readiness

Partners with defined ICPs, packaged offers, and consistent messaging are easier to activate. They don’t need to be taught how to sell from scratch—they need direction on where and when to engage. This reduces time to first deal and lowers enablement overhead.

2. Proven capabilities and use cases

For SIs, this shows up as relevant certifications and delivery depth. For ISVs, it’s tight integrations, proof points, and customer outcomes. Partners that can point to where they’ve already won—and what changed for the customer—are far more likely to be trusted in live deals.

3. Early co-sell traction

You don’t need massive revenue to see momentum. A handful of qualified opportunities, joint pipeline reviews, or early wins indicate the partner understands how to execute within the ecosystem. These partners have crossed the hardest threshold: moving from theory to motion.

4. Field advocacy

Perhaps the strongest signal is seller behavior. When AEs proactively invite a partner into accounts, reference them internally, or advocate for their inclusion, it reflects earned trust. Field backing amplifies everything else—reach, credibility, and velocity.

These signals compound. A partner with a strong use case and an AE champion is a very different investment than one with credentials alone.

A simple way to prioritize without over-engineering

You don’t need complex scoring models. A lightweight rubric works:

Tier 3 (Baseline): Partial GTM clarity, minimal traction, little field awareness

Tier 2 (Emerging): Solid positioning, some use cases, early co-sell activity

Tier 1 (Invest): Packaged for the field, proven outcomes, active AE advocacy

The goal isn’t permanence. It’s movement.

What vendors should do next

Map and monitor signals using deal activity, certifications, and pipeline data.

Bring the field into evaluation by asking which partners they trust and why.

Align investment to readiness, not logos—deeper focus for Tier 1, structured nurture for Tier 2, foundations for Tier 3.

Reassess regularly so partners can earn their way up.

The takeaway

High-performing ecosystems don’t grow by treating every partner the same. They grow by recognizing where momentum already exists—and concentrating effort there. When investment follows real signals of readiness and trust, partner programs stop being a cost center and start behaving like a scalable revenue engine.

From Credibility to Pipeline: Making Partner-Led Growth Real

Strong GTM positioning and credible capabilities earn partners a seat at the table. But credibility alone doesn’t produce revenue. Pipeline appears only when vendors intentionally design how partners, AEs, and opportunities come together in real deals.

This is where many ecosystems stall. Partners are “ready,” but co-selling remains inconsistent, late, or symbolic. The difference between ecosystems that scale and those that plateau is execution.

Co-selling works when it’s operationalized. Done well, it shortens sales cycles, improves win rates, and increases deal size. Done poorly, it becomes a buzzword with no behavioral change.

Turning credibility into pipeline requires a few deliberate moves.

Strong GTM positioning and credible capabilities earn partners a seat at the table. But credibility alone doesn’t produce revenue. Pipeline appears only when vendors intentionally design how partners, AEs, and opportunities come together in real deals.

This is where many ecosystems stall. Partners are “ready,” but co-selling remains inconsistent, late, or symbolic. The difference between ecosystems that scale and those that plateau is execution.

Co-selling works when it’s operationalized. Done well, it shortens sales cycles, improves win rates, and increases deal size. Done poorly, it becomes a buzzword with no behavioral change.

Turning credibility into pipeline requires a few deliberate moves.

1. Map accounts and opportunities early

Effective co-sell starts before deals exist. Joint account mapping surfaces where partners and sellers overlap—and where collaboration actually makes sense. When partners know which accounts matter and why, engagement shifts from reactive to proactive.

Late-stage partner introductions rarely change outcomes. Early alignment does.

2. Align the field on when and how to co-sell

Most AEs aren’t resistant to partners—they’re unclear on the motion. Co-sell works when sellers understand:

what problem the partner helps solve

when to bring them into a deal

what role each party plays

Targeted enablement focused on real scenarios—not generic partner overviews—creates confidence and repeatability.

3. Remove friction from pipeline visibility

If deal registration is slow, confusing, or disconnected from seller workflows, it won’t be used. Co-sell accelerates when partners and AEs can see the same opportunities, track progress together, and understand how collaboration impacts outcomes.

Visibility isn’t about reporting after the fact. It’s about alignment while deals are live.

4. Reinforce success publicly and often

Co-sell becomes cultural when success is visible. Highlighting wins—who collaborated, what worked, and why—signals that partner engagement is valued and expected. Over time, this shifts behavior from one-off experimentation to habit.

5. Segment for scale

Not every seller or partner needs the same level of support. Segment by readiness and performance. Focus deeper enablement on those actively co-selling, while providing lighter guidance to others. Scale comes from focus, not uniformity.

The takeaway